April 29, 2026 | Ali Bolourchi — The Visionary Curator

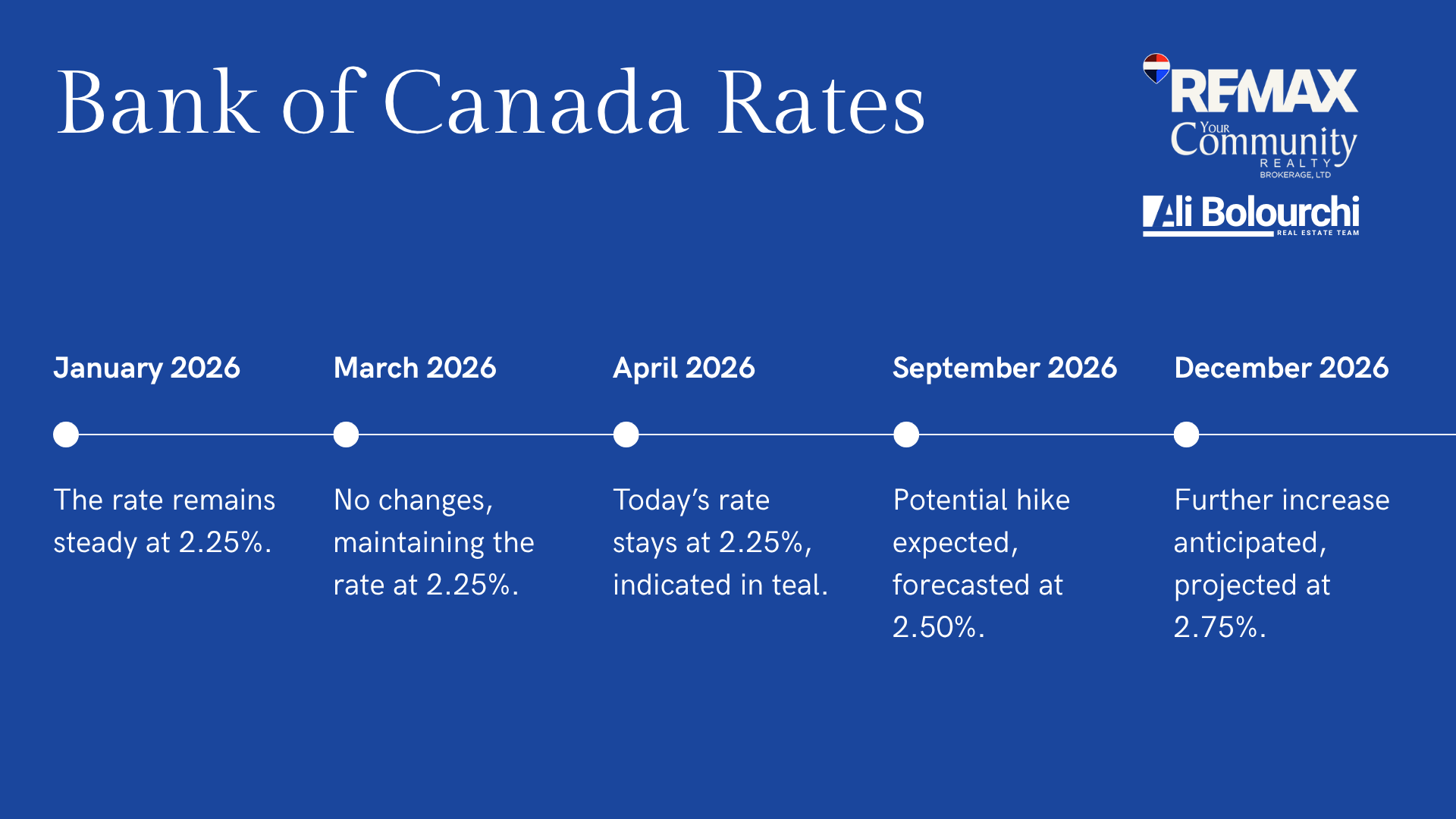

Today the Bank of Canada did exactly what most economists expected: nothing. The overnight rate stays at 2.25%, held for the third consecutive time in 2026. But beneath that quiet headline, a much bigger story is unfolding in the Canadian housing market. One that will reshape who can afford what, who decides to sell, and who finally pulls the trigger on a purchase.

If you own property in the GTA, are thinking of listing, or have a mortgage coming up for renewal, this decision matters — more than the headline suggests.

Why the Bank Held — And Why It's More Complicated Than It Looks

The Bank of Canada isn't holding rates because the economy is in great shape. It's holding because it's caught between two competing forces pulling in opposite directions:

Inflation came in at 2.4% in March — up sharply from 1.8% in February — and the Bank is already warning it could climb to around 3% in April. Much of that pressure is coming from energy costs tied to the ongoing conflict in the Middle East, which has disrupted supply chains and pushed oil prices higher. At the same time, U.S. tariff uncertainty is weighing on Canadian exports and business investment, acting as a brake on growth. GDP is forecast at just 1.2% for 2026 — cautious, not confident.

Cut rates, and you risk feeding inflation further. Hike rates, and you risk choking an already fragile recovery. So the Bank sits still — and watches.

A Reuters poll of 41 economists found 100% expected today's hold, and 80% believe rates won't move for the rest of 2026. But a minority are pricing in two quarter-point hikes — possibly in September and December — if inflation proves stickier than the Bank expects.

The Renewal Wave: The Real Story Behind Today's Decision

Here's what makes this particular rate hold so consequential: approximately 60% of all outstanding Canadian mortgages are renewing in 2025 or 2026. In 2026 alone, roughly 1.2 million fixed-rate mortgages — representing over $300 billion in debt — are hitting renewal.

These are homeowners who locked in when the overnight rate was near zero and 5-year fixed rates sat between 1.5% and 2.5%. They are now renewing into a world where the best available 5-year fixed rate is 4.04% through a broker, or 4.29% at a major bank. The lowest 5-year variable is around 3.35%.

The financial impact, what analysts are calling "payment shock", breaks down roughly like this: the majority of 5-year fixed renewers will see monthly payments rise by an average of 20%. For a $750,000 mortgage, that's an additional $400–$600 every single month. The hardest-hit 10% of borrowers will see payments jump by more than 40%. The silver lining belongs to variable-rate holders, who may actually see a modest 5–7% decrease.

What This Means for GTA Sellers

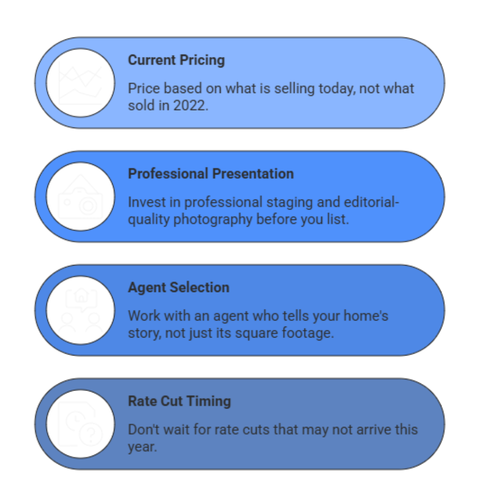

The rate hold is a quiet opportunity — but only for sellers who treat it that way.

Stable rates give buyers a clearer picture of what they can afford. The "what if rates spike again?" anxiety fades, and fence-sitters begin to move. That's good for sellers. What's less good: inventory has been building steadily in the GTA through early 2026, giving buyers more choices and more leverage than they've had in years.

In this environment, the homes that sell — and sell well — are not the ones that are simply listed. They are the ones that are curated, priced with precision, and presented as a lifestyle rather than a property. The renewal wave is also quietly adding supply: homeowners who can't absorb a $500/month payment increase at renewal are starting to list. Your competition is growing.

The sellers who will win in this market are those who come in prepared and presented. Not those who "test the water" with an aspirational price and hope the market comes to meet them.

The seller's checklist right now:

What This Means for GTA Buyers

Today's hold is quietly good news for buyers — even if it doesn't feel that way yet.

Rate stability means your pre-approval holds its value. You can model your payments with confidence. And the inventory that has accumulated in the GTA gives you something that was almost impossible to find two years ago: genuine choice and real negotiating power.

Variable rates deserve serious consideration right now. At 3.35% for a 5-year variable, buyers comfortable with some flexibility are accessing meaningfully lower payments than fixed-rate options — and if the Bank holds through the year as most economists expect, that advantage compounds.

The window is real, but it's not guaranteed to stay open. If inflation persists and the Bank does move in the fall, the affordability equation shifts again. Buyers who act in Q2 and Q3 2026 are buying into relative clarity. Buyers who wait for the "perfect" rate may find the window has closed.

This is the market where you negotiate conditions, price, and closing terms. Use it.

What This Means for GTA Investors

Investors need to run the numbers — honestly — before making any move.

The renewal math is brutal for properties financed at pandemic-era rates. A rental that cash-flowed at 2% needs to be stress-tested at 4%+. If it doesn't work on paper today, holding and hoping isn't a strategy.

The condo market in the GTA deserves particular scrutiny. TD Economics has flagged it as facing continued headwinds — oversupply, softening rents in some pockets, and price stagnation. If your exit strategy was "sell into a rising market," it's time to reassess whether that market exists right now for condos.

Where genuine opportunity lies: the renewal wave is creating motivated sellers — homeowners who need to transact, not those who simply want to. Freehold properties in established GTA neighbourhoods continue to hold value better than the condo segment. Investors with dry powder and patience are entering the best buying environment in years.

The long-term case for GTA real estate — population growth, immigration, chronic undersupply — hasn't changed. But short-term decisions need to be made on current data, not long-term faith.

The Bottom Line

The Bank of Canada's decision to hold at 2.25% is not a green light or a red flag. It's a pause — a moment of unusual clarity in an otherwise volatile economic picture.

For the GTA real estate market, the real story isn't the rate decision itself. It's what's happening beneath it: a massive renewal wave is quietly forcing decisions, adding inventory, shifting buyer calculus, and creating opportunities for those who are paying attention.

The sellers who read this market correctly will price with discipline and present with intention. The buyers who read it correctly will act with confidence rather than waiting for a rate that may never arrive. The investors who read it correctly will make decisions rooted in today's numbers — not yesterday's optimism.

If you want to understand exactly what today's announcement means for your specific situation — whether you're listing, buying, or stress-testing a portfolio — I'm here.

Ali Bolourchi | The Visionary Curator | [email protected]

.png)